About Girin Market Models

|

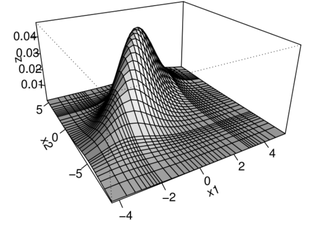

MNTS distribution and copula: The dependence structure in asset returns is explained by the correlation in classical finance. However, asset returns have asymmetric dependence which is not described by correlation. The MNTS distribution can capture the asymmetric dependence. The captured asymmetric dependence can be visually expressed by the MNTS copula.

|

|

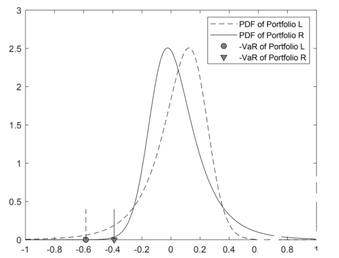

Risk and Distribution: Suppose that Portfolio L has the left-skewed return distribution and Portfolio R has the right-skewed return distribution. Then Portfolio L is riskier than Portfolio R. The figure graphically explains that fact. |

Application of Girin Market Models

|

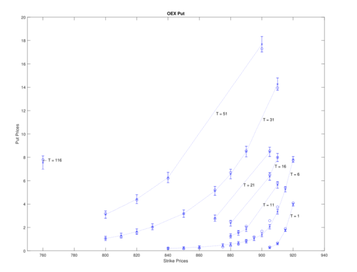

American option pricing and calibration: Using a Girin Solution, we can develop a more accurate simulation method to describe the American option price. |

|

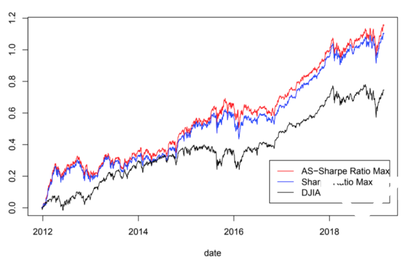

Horse racing of the portfolio performance: Considering the dispersion risk and asymmetric risk, we obtain a portfolio (red curve) that has better performance than DJIA (black curve) and Sharpe-ratio minimizing portfolio (blue curve). |

|

|

An in-depth guide to understanding probability distributions and financial modeling for the purposes of investment managementIn Financial Models with Lévy Processes and Volatility Clustering, the expert author team provides a framework to model the behavior of stock returns in both a univariate and a multivariate setting, providing you with practical applications to option pricing and portfolio management. They also explain the reasons for working with non-normal distribution in financial modeling and the best methodologies for employing it.

https://a.co/d/5ttuUZY |

Copyright 2021. Girin Instruments all rights reserved.